Table of Contents▼

"The budget is not merely a technical presentation of numbers, nor is it only an 'economic-political document.' It is a reliable map of the path to making the country better and better."

— Finance Minister Dr. Swarnima Wagle, Budget Speech §79, FY 2083/84

The Finance Minister is right that a budget is a map. But maps and terrain are different things. Nepal has produced ambitious maps before.

This article is not a summary of the FY 2083/84 budget — there are dozens of those already. It is an institutional reading: a structured attempt to separate what is structurally new from what is repackaged, what has legislative backing from what is ministerial intent, and what private capital and project developers should act on now versus watch carefully from a distance.

We write this as practitioners in project finance, SPV structuring, and regulatory compliance in Nepal — not as commentators. Our assessment is calibrated accordingly.

The Headline Numbers in Context

| Metric | FY 2083/84 Budget | Prior Year Revised |

|---|---|---|

| Total Budget | NPR 2,124.34 billion | NPR 1,696.01 billion |

| Growth vs. Prior Year | +25.2% | — |

| Capital Expenditure | NPR 431.10 billion (20.3%) | NPR 251.40 billion |

| Recurrent Expenditure | NPR 1,270.58 billion (59.8%) | — |

| Revenue Target | NPR 1,405.31 billion | NPR 1,300.23 billion |

| Fiscal Deficit | NPR 657.29 billion | — |

| GDP Growth Target | 7% | 3.85% actual (2082/83) |

The 25.2% budget expansion is the largest single-year increase Nepal has announced in recent memory. At face value, it signals a government willing to put institutional weight behind its reform rhetoric.

At second glance, it raises the central question of this analysis.

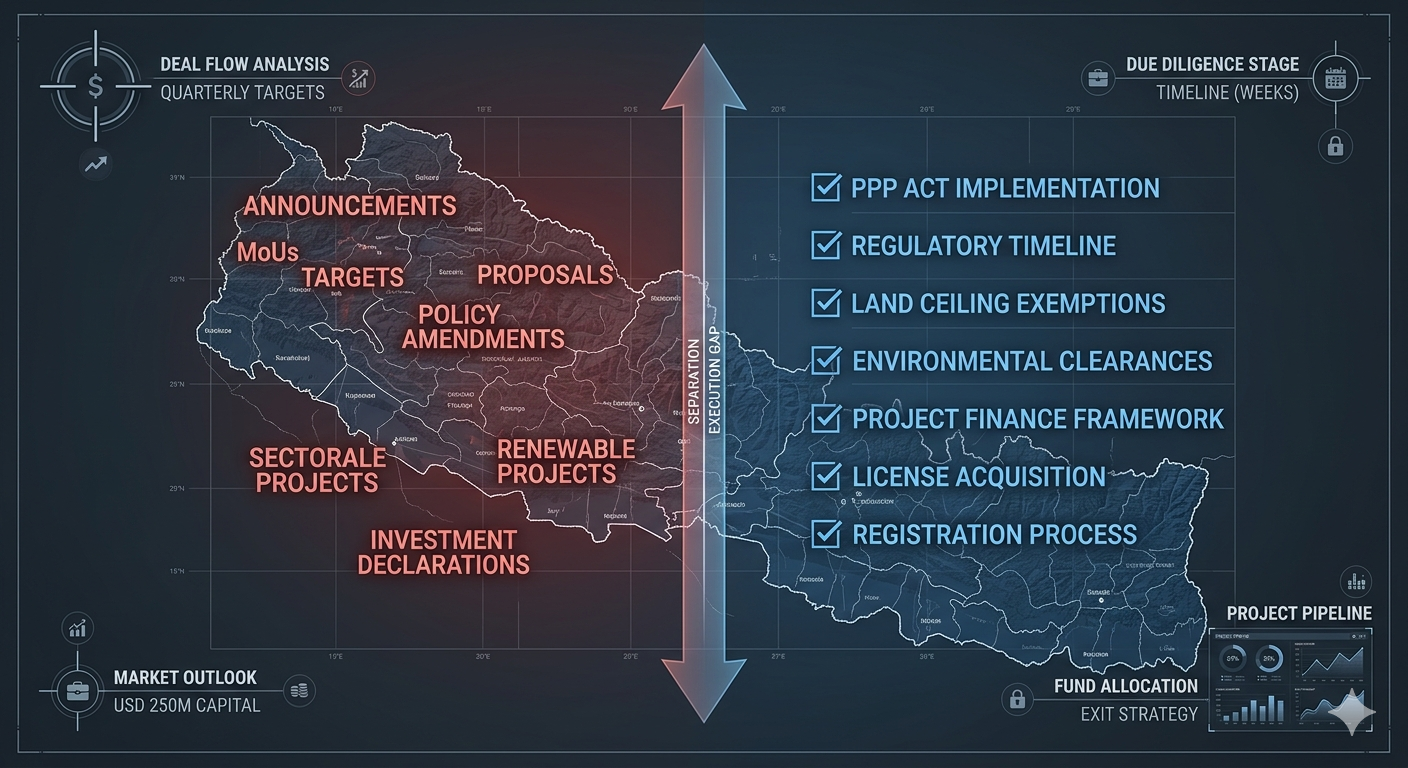

The Execution Gap: A Structural Problem, Not a Political One

Before evaluating what is new in this budget, the reader must understand what is historically true about Nepal's capital budgets.

In FY 2080/81, Nepal spent only 41.67% of its capital budget by May — a month before fiscal year close. In FY 2081/82's second quarter, the capital expenditure rate was 23.37% against an expected 50% midpoint. These are not anomalies. They are the baseline.

This is not a criticism of any particular government. It reflects structural bottlenecks that have persisted across political cycles:

- Procurement timing: The bulk of capital spending has historically occurred in the final two months of the fiscal year — Ashadh rush spending — producing poor quality outcomes, contractor defaults, and incomplete works.

- Forest and land clearance delays: EIA approvals, tree-felling orders, and forest clearance remain multi-agency bottlenecks that stall infrastructure projects for years post-approval.

- Project chief instability: Frequent transfers of project chiefs disrupt institutional memory and contractor relationships mid-execution.

- Lowest-bid procurement: Nepal's procurement framework has historically prioritized lowest bid over contractor capacity, producing delayed delivery and cost overruns.

The FY 2083/84 budget acknowledges several of these directly — the EIA amendment (§13), project chief stability commitment (§11), and sunset law for stalled projects (§11) are all responses to known structural failures.

What's different this time is the political mandate behind these provisions. The Balendra Shah-led RSP government entered with a near-supermajority on an explicitly reform-oriented platform. The Finance Minister has presented not just a budget but a governance thesis. That is genuinely new.

What's not different is the implementation infrastructure. The civil service, procurement agencies, DFI coordination mechanisms, and project management offices executing this budget are largely the same institutions that produced those historical underperformance numbers. A 25.2% budget expansion with unchanged implementation capacity is either an opportunity or a liability — depending entirely on how the first six months of FY 2083/84 play out.

Five Provisions That Matter Most for Private Capital

Filtered from 80 budget paragraphs and 15 annexures, these are the provisions with the highest direct relevance for PE/VC investors, domestic project developers, and DFIs operating in Nepal.

1. NEA Unbundling — The Most Consequential Structural Reform in a Decade

"Nepal Electricity Authority will be divided into three separate companies for power generation, transmission, distribution and trading." — Budget §19

This is not a new idea. NEA unbundling has been discussed in Nepal's energy policy for over fifteen years. What is new is a finance minister with a strong mandate presenting it as a committed budget provision rather than a policy aspiration.

If implemented, it creates three distinct counterparties where one existed before — with significant implications for:

- PPA structures: Which entity signs power purchase agreements going forward? The generation company, or the trading company?

- Wheeling arrangements: Who holds transmission rights and at what tariff structure?

- SPV equity governance: How do projects with existing NEA offtake agreements manage the transition period?

The candid assessment: The transition period is the risk. Unbundling NEA requires parallel legislative amendments, staff redeployment across three new entities, and new regulatory frameworks for inter-company transfer pricing. Historically, institutional restructurings of this scale in Nepal have taken 3–5 years to operationalize. Developers with projects in pre-financial-close or mid-construction should seek explicit contractual clarity on counterparty continuity before the restructuring begins.

2. FITTA Amendment — Investment Architecture Shifts

"The Foreign Investment and Technology Transfer Act will be amended to allow repatriation of investment without prior Nepal Rastra Bank approval — notification sufficient. Foreign investment coverage extended to convertible instruments, project-linked funding, and other hybrid instruments." — Budget §10(b)

This matters. The prior approval requirement for repatriation was a documented friction point for foreign PE/VC and DFI capital — not because approval was typically withheld, but because the process created timing uncertainty that complicated fund-level return modelling.

The extension to convertible instruments and hybrid structures is equally significant. It opens the door to SAFE notes, convertible debt, and project-linked financing structures that were legally ambiguous under the existing FITTA framework.

The candid assessment: Nepal has amended FITTA before — most recently in 2019 — with positive intent that produced uneven implementation. The prior amendment's regulations and directives took 18+ months to fully publish after the Act was passed. The Act amendment is not the finish line; the NRB directives implementing the "notification sufficient" regime are. Investors should monitor NRB circular issuance, not just Parliamentary passage of the amendment.

3. Private Sector Cross-Border Electricity Trade Rights

"Private sector players will be allowed to trade electricity in international markets — including the right to build transmission lines and charge wheeling fees." — Budget §20

This is the single provision most likely to unlock a new PE/VC infrastructure asset class in Nepal if implemented as written. It creates the legal basis for privately-owned transmission infrastructure with a revenue model — wheeling fees — that is fundable by institutional capital.

The cross-border context matters: the Butwal–Gorakhpur and Inaruwa–Purnia transmission lines to India are already progressing. Bangladesh discussions are active. A private developer with a transmission line and wheeling fee rights could, in theory, build a revenue-generating infrastructure asset outside the NEA balance sheet entirely.

The candid assessment: The right to build transmission lines has appeared in Nepali energy policy documents before without producing private-sector transmission infrastructure. Two structural barriers remain: land acquisition for transmission corridors (a chronic bottleneck in Nepal's infrastructure development) and the regulatory framework for wheeling tariff determination, which does not yet exist. The provision is directionally correct and potentially transformative — but the enabling regulatory architecture needs to be published before capital commits.

4. Capital Markets Modernisation — Final Tax on Listed Shares, GDRs, NRN Access

Three capital market provisions in §36 and §10(d) collectively represent the most significant opening of Nepal's securities market to institutional and diaspora capital in years:

- Capital gains as final tax removes uncertainty for investors in listed companies — particularly relevant for hydropower SPVs planning IPO exits.

- Global Depositary Receipts for NEPSE-listed companies creates a legal pathway to foreign listing and international capital raising.

- NRN secondary market access formalises diaspora participation in listed securities.

The candid assessment: NEPSE's current market infrastructure — settlement systems, custodian arrangements, foreign exchange repatriation pipelines — is not yet GDR-capable. The provision creates the legal right before the operational infrastructure exists to exercise it. The NEPSE restructuring promised in §36 (intraday trading, short-selling, derivatives) requires parallel technology investment and regulatory rulemaking. These are medium-term wins that are unlikely to be operational within FY 2083/84 but represent a credible direction of travel for the first time.

5. Alternative Development Finance — Sovereign Fund, Offshore Bonds, Climate Finance

"Offshore bonds in Nepali currency will be issued in international markets. Clean Energy Bonds and Diaspora Bonds will be issued, and available climate funds will be maximised. A 'Motherland Fund' (Matribhumi Kosh) will be established to invest in strategic projects such as minimum three-month fuel storage and an AI Factory." — Budget §14–15

This cluster of provisions represents Nepal's most ambitious attempt yet to mobilise capital outside the government balance sheet. The logic is sound: Nepal's debt-to-GDP is rising, foreign grants are declining (Annexure 11 shows multilateral grant share declining relative to loans), and domestic borrowing at NPR 41 billion gross has limits.

Clean Energy Bonds and Diaspora Bonds, if structured correctly, tap two deep pools of capital that have historically flowed to Nepal informally — international climate finance and remittances — and formalise them into investable instruments.

The candid assessment: The credibility of these instruments in international markets will depend entirely on what verification and reporting architecture sits underneath them. A "Clean Energy Bond" issued without internationally legible ESG certification, independent project verification, and transparent use-of-proceeds reporting will not price competitively. Nepal does not currently have that institutional infrastructure at scale. This is not insurmountable — but it requires deliberate infrastructure investment before the instruments are issued, not after.

The Structural Shifts That Don't Get Enough Attention

Beyond the headline provisions, three budget signals deserve more attention than they are receiving in current commentary.

The Government Right-Sizing Is Real and Has Cash Implications

The abolition of 31 agencies, merger of 6, and restructuring of 18 is projected to save NPR 20 billion (§9). That number sounds modest against a NPR 2,124 billion budget. But the institutional signal is significant: this is a government willing to dismantle patronage infrastructure. For private developers who have historically navigated overlapping agency approvals, a leaner federal structure — if it holds — reduces transaction costs that don't appear in any project financial model but are very real.

The Investment Express System Is a Compliance Architecture, Not Just a Window

The Investment Express system (§26) is described as a single-platform integration of company registration, financial services, tax, and visas. If implemented as described — with approved projects exempted from further agency approvals — it fundamentally changes the project development timeline for Investment Board-approved projects. Currently, IBN approval does not prevent projects from facing additional clearances from sector ministries, municipalities, and technical agencies. If the "no further approvals" commitment is enforced, it removes years from pre-construction timelines.

The LLP Law Could Reshape Nepal's Entire Early-Stage Capital Ecosystem

The Limited Liability Partnership law (§10a) is a single line in an 80-paragraph budget speech. It will receive almost no commentary. It is potentially among the most consequential provisions for Nepal's PE/VC ecosystem.

Currently, fund structures in Nepal are awkward — most operate through company structures that create inappropriate tax treatment for carried interest and complicate LP/GP governance. A properly drafted LLP law creates the legal vehicle for Nepal-domiciled PE/VC funds that can raise capital from domestic institutional investors (EPF, CIT, insurance companies) in a tax-efficient structure. The downstream effects on early-stage capital availability could be significant.

What to Watch in the First 90 Days

The FY 2083/84 budget is presented. The FY begins Shrawan 1. The most meaningful signal of implementation intent will come from the following observable events in the first quarter:

| Indicator | What to Watch | Why It Matters |

|---|---|---|

| Investment Express | Live by Aswin (3 months post-budget)? | Stated commitment; tests execution speed |

| FITTA Amendment Bill | Parliamentary tabling timeline | Amendment without bill is noise |

| NEA Unbundling | Formation of transition committee | Process signal for timeline |

| NRB Directives | Fintech Marketplace, P2P framework | Regulatory infrastructure for new provisions |

| Capital Expenditure Rate | Shrawan–Kartik spending pace | Tests whether Ashadh-rush pattern is broken |

| National Asset Management Company | Established by Poush (stated)? | NPL resolution has systemic banking implications |

The Institutional Verdict

This budget is the most reform-oriented Nepal has presented in at least a decade. It earns that designation not primarily for its size but for the coherence of its institutional logic: the tax simplification, government right-sizing, investment facilitation, and capital market opening provisions fit together as a systemic package rather than a collection of sectoral announcements.

The government that produced it has a genuine political mandate for reform — something its recent predecessors did not.

What it is not is a transformation delivered. It is the most credible blueprint Nepal has produced for a transformation it has attempted, in various forms, for twenty years.

For PE/VC investors and project developers, the posture we recommend is structured optimism with milestone-gated commitment:

Watch the first 90 days of capital expenditure execution. Watch the FITTA amendment's implementing regulations, not just the Act. Watch the NEA restructuring timeline before restructuring your SPV models. Watch the Investment Express go-live date.

Nepal's reform story is genuinely compelling right now. The government deserves credit for the ambition and coherence of this budget.

The terrain, however, still needs to match the map.

About Silicon Himalayas

Silicon Himalayas is a project finance and advisory firm working on feasibility studies, SPV structuring, regtech compliance, and blockchain-based green verification for energy and infrastructure projects in Nepal.

We operate across 20 Expert Committees spanning Energy & Environment, Infrastructure & Urban Development, Finance/Law/Governance, and Sectors & Social domains.

Explore our services → Read more Insights →

The views expressed in this article represent Silicon Himalayas' independent analytical assessment and do not constitute investment advice.